Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

8

September 2025 Alabama Gulf Coast Real Estate Stats

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

September 2025 Recap

As we moved into September, both Baldwin and Mobile Counties showed signs of a shifting market that's settling into fall. Across Baldwin County, steady sales activity kept most areas balanced, with hotspots like Daphne, Fairhope, and Foley maintaining healthy momentum. Coastal markets such as Gulf Shores and Orange Beach saw the usual seasonal slowdown, especially in the condo sector. Meanwhile, Mobile County followed a similar pattern—mid-range homes in areas like Midtown, Springhill, and West Mobile continued to move, while higher-end and outlying markets experienced a modest cooling. Overall, both sides of the Bay remain stable, offering opportunities for buyers and sellers alike as we transition into the final stretch of 2025.

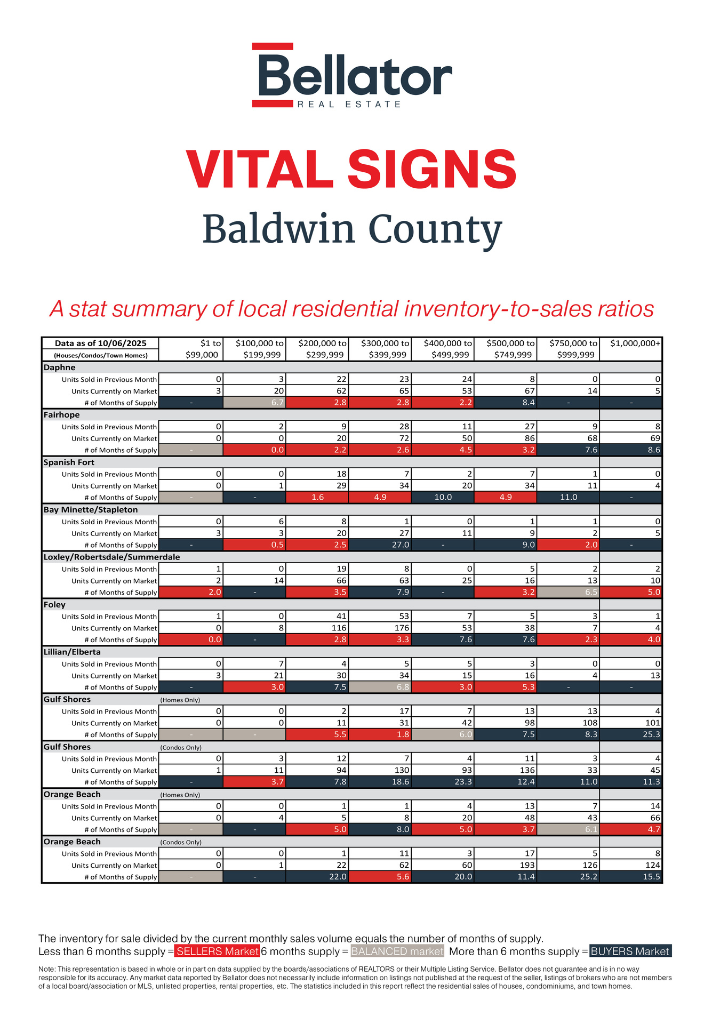

Baldwin County Market Update — September 2025

Balancing Act: A Cooling Trend with Notable Shifts in Coastal and Eastern Markets

Baldwin County's September housing data shows a market continuing to balance between supply and demand, with subtle but important shifts across price ranges and communities. While total listings remain elevated compared to mid-summer, buyer activity has stayed steady in many areas—keeping several markets in the three to four months of supply range, signaling a continued lean toward balance rather than a full buyer's market.

Eastern Shore Markets Stay Active, but Begin to Ease

In Daphne, inventory held steady while closings dipped slightly compared to August. The months of supply stayed balanced around 2.8 to 3 months for most price ranges, reflecting continued buyer demand but at a slower pace than mid-summer.

Fairhope remains one of the more competitive submarkets, with modest inventory growth paired with strong sales in the mid-range price points ($300K–$600K). The months of supply decreased in several brackets, keeping Fairhope attractive for sellers who price strategically.

Spanish Fort, however, saw a notable slowdown, especially in the $300K–$400K range, where supply climbed to nearly five months. This suggests buyers in that segment have more breathing room than they did earlier in the summer.

Rural Markets Hold Steady

In Bay Minette and Stapleton, activity picked up slightly in lower price ranges, pushing supply down to 2.5 months in the $200K–$300K bracket—an improvement over August's 5.8 months. Meanwhile, higher price ranges saw fewer transactions, keeping those brackets more saturated with inventory.

Loxley, Robertsdale, and Summerdale remained consistent month over month. With 3–4 months of supply in the $200K–$500K ranges, these communities reflect a stable balance where both buyers and sellers can negotiate confidently.

Coastal Markets See Mixed Movement

On the coast, trends were more mixed:

- Gulf Shores (Homes Only) saw a sharp jump in closings—especially in the $300K–$400K range, where months of supply dropped to just 1.8 months, compared to 8.6 months in August. That's one of the most significant month-to-month improvements countywide.

- Gulf Shores Condos, by contrast, cooled down. Supply increased in nearly every price tier, with months of supply rising to 18.6 months in the $300K range and 23.3 months in the $400K range.

- Orange Beach Homes saw a healthy boost in transactions across several brackets, cutting months of supply in half in many categories.

- Orange Beach Condos mirrored Gulf Shores' condo trend, with rising inventory and slower sales—suggesting that the second-home and investment segments are adjusting as the fall season begins.

Overall Takeaway

September's data points to a more balanced market than we've seen all year. Demand remains solid in core residential areas like Daphne, Fairhope, and Foley, while the luxury and coastal segments are seeing longer marketing times and increased supply.

Buyers now have more options without the aggressive competition of early summer, and sellers can still achieve strong results by pricing within the most active ranges—typically under $500K in most Baldwin County communities.

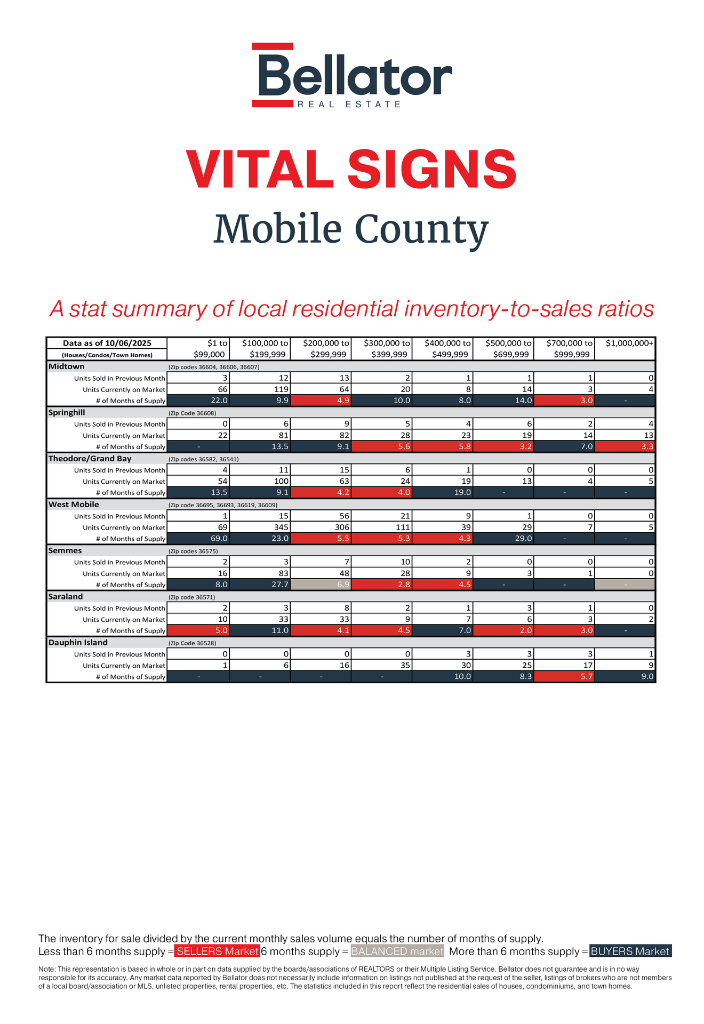

Mobile County Market Update — September 2025

Steady Sales and Seasonal Shifts Define Early Fall Market

Mobile County's housing market in September reflected a mix of stability and seasonal slowdown, with buyer activity remaining steady in core residential areas while higher-end and coastal segments began to ease into fall pacing. Compared to August, several markets posted stronger sales in affordable price ranges, while others saw slight increases in supply—a sign that the market continues to move toward balance after a busy summer.

Midtown and Springhill: Balanced but Cooling

In Midtown, homes priced under $300,000 remained in high demand. Inventory dropped modestly in most brackets, and months of supply improved — especially in the $200K–$300K range, which moved from 6.8 months in August to 4.9 months in September. However, higher price points saw a slower pace, with $400K–$500K homes sitting longer at 8–10 months of supply.

Springhill experienced a similar pattern: steady movement in mid-range homes, while the luxury bracket softened slightly. September saw balanced conditions in the $300K–$600K range (around 5–6 months of supply), suggesting solid buyer engagement and steady turnover in one of Mobile's most desirable areas.

West Mobile: Slight Cooling After a Busy Summer

West Mobile, one of the county's most active markets, saw a slight dip in sales volume compared to August. While inventory held steady, the months of supply in the $200K–$400K range rose slightly to around 5–5.5 months, signaling a more even playing field between buyers and sellers. Homes priced below $200K remain competitive, though that segment did see a jump in months of supply from 14.5 to 23.0 months, as listings accumulated faster than closings.

Southern Markets Show Varied Trends

In Theodore and Grand Bay, supply stayed relatively stable overall, with September posting similar levels of activity to August. Homes in the $200K–$400K range continued to perform well, hovering around 4 months of supply, while higher-priced homes above $500K are lingering longer, typical for the fall season.

Dauphin Island continues to show the strongest seasonal influence, with very few sales recorded in September after a modestly active August. Inventory remains steady, but slower movement in vacation and waterfront properties pushed most price ranges above 8 months of supply, indicating a clear shift toward a fall and winter buyer's market.

North Mobile: Steady Demand Holds in Affordable Segments

The Semmes market held consistent with late-summer trends, particularly in homes priced below $400K, where months of supply remained around 3–7 months. Higher price points remain sparse in both listings and closings, a reflection of Semmes' largely affordable housing base.

In Saraland, another stable performer, supply tightened slightly in the mid-range brackets. Homes priced between $300K–$500K stayed balanced at around 4–5 months of supply, showing steady buyer interest. The higher-end segment over $700K remains thinly traded but not over-saturated.

Overall Takeaway

Mobile County's September data highlights a more balanced, steady market as fall begins. Entry-level and mid-range homes remain the most active price points across nearly every submarket, while upper-tier and coastal properties are seeing typical seasonal slowdowns.

For sellers, pricing remains key—especially as buyers gain a bit more leverage with increased inventory. For buyers, the fall market is offering more choice and less competition than the high-speed months of spring and summer.

Whether you're entering as a buyer or seller, knowing your segment and working with a Bellator Real Estate advisor ensures you're positioned strategically in this changing market.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.

Privacy Policy / DMCA Notice / ADA Accessibility