Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

10

October 2025 Alabama Gulf Coast Real Estate Stats

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

October 2025 Recap

As fall settles across Alabama's Gulf Coast, both Baldwin and Mobile County housing markets are showing signs of seasonal balance. Inventory levels remain steady across most price points, while demand continues to normalize after the busier summer months. Mid-range homes are seeing the strongest movement as buyers and sellers adjust to a more sustainable pace, and higher-end properties continue to draw selective but serious activity. From coastal condominiums to suburban family homes, both counties reflect a market finding its rhythm heading into the final quarter of 2025.

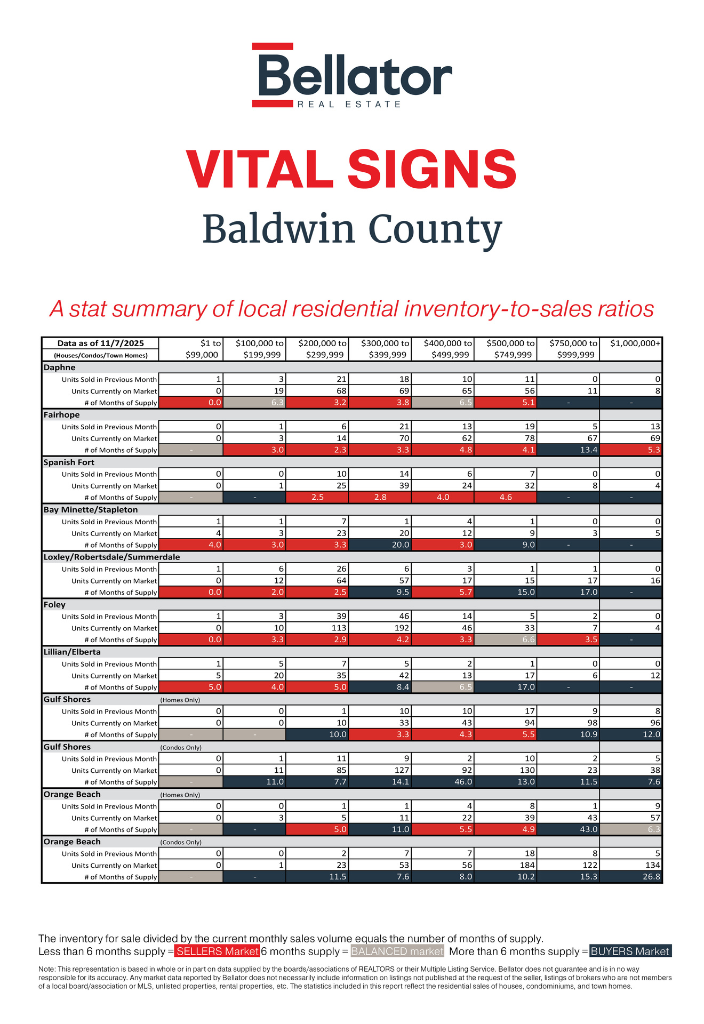

Baldwin County Market Snapshot: September vs. October 2025

The market continued its seasonal shift in Baldwin County, with inventory levels holding steady in most areas while sales activity began to taper slightly—a typical trend for fall along the Gulf Coast. However, several markets, particularly along the Eastern Shore, saw notable changes that could set the tone for year-end.

Eastern Shore Market Overview

- Daphne

Daphne's housing market stayed relatively balanced but showed a small slowdown in sales volume compared to September. The number of homes sold fell from 80 to 64 overall, and months of supply ticked up in most price ranges—especially between $300K–$500K, where supply rose from around 2–3 months to 3–6 months. This indicates a gradual move toward a more neutral market, giving buyers slightly more room to negotiate. - Fairhope

Fairhope's luxury segment showed interesting movement. Homes priced $750K–$999K and $1M+ saw basically a wash in supply (13.4 and 5.3 months, respectively), suggesting continued softening at the top end. Meanwhile, mid-range homes between $300K–$500K maintained solid turnover, with months of supply hovering between 3–5 months—a sign that demand remains strong for well-priced listings. - Spanish Fort

Spanish Fort saw a shift in balance as well—particularly in the $300K–$400K range, where supply decreased from nearly 5 months in September to just 2.8 months in October. Homes priced above $500K remained stable, though lower sales numbers indicate that demand is concentrated in the mid-range sector.

North Baldwin & Central County

- Bay Minette and Stapleton

This submarket experienced a rebound in sales under $400K, bringing months of supply down from extreme highs (27 months in September for the $300K–$399K range) to a more moderate 20 months in October. While that's still a slower pace, it's an improvement—signaling better absorption of listings as prices adjust. - Loxley, Robertsdale, and Summerdale

These communities continued to attract steady buyer interest. Homes under $300K performed well, keeping supply tight at 2–3 months, though higher price points saw a jump in inventory—particularly in the $500K+ category, where supply increased sharply to 15–17 months. This indicates that while entry-level homes remain competitive, luxury inventory is lingering longer.

Southern Baldwin County & Coastal Markets

- Foley

Foley maintained a healthy balance through October, with most price points seeing minimal change. Homes in the $300K–$400K range remain in high demand, and months of supply only rose slightly from 3.3 to 4.2 months. Overall, Foley continues to offer one of the most balanced markets in Baldwin County. - Lillian & Elberta

Inventory increased slightly across most ranges, pushing supply higher—especially above $500K, where months of supply reached 17 months. While that may seem high, it's consistent with seasonal trends in these more rural, slower-moving submarkets. - Gulf Shores & Orange Beach (Homes)

Both Gulf Shores and Orange Beach single-family markets showed the typical off-season cooling. In Gulf Shores, the $750K–$1M range rose from 8.3 months to 10.9 months of supply, while Orange Beach homes above $1M climbed to 6.3 months, indicating slower movement in luxury coastal homes. - Gulf Shores & Orange Beach (Condos)

The condo market along the coast also continues to reflect the seasonal ebb and flow. Supply in Gulf Shores condos rose significantly in the $400K–$499K segment (from 23 months to 46 months), signaling reduced absorption after the busy summer season. Orange Beach condos followed a similar path, with the $1M+ tier now sitting at 26.8 months of supply, up notably from 15.5 months in September.

Despite these increases, the trend is typical for October—as the tourism and second-home buying season winds down, listings often sit longer until early spring demand returns.

Key Takeaways

- Inventory levels are holding steady, with slight increases in the luxury and coastal segments.

- Mid-range homes ($300K–$500K) remain the most active and balanced price point countywide.

- Seasonal cooling is evident, particularly in Gulf-front condo markets and upper-tier homes.

- Buyers are regaining leverage, with more options and longer days on market expected through winter.

As the market eases into the final months of 2025, Baldwin County remains a study in balance; still active, but less frenetic than earlier this year.

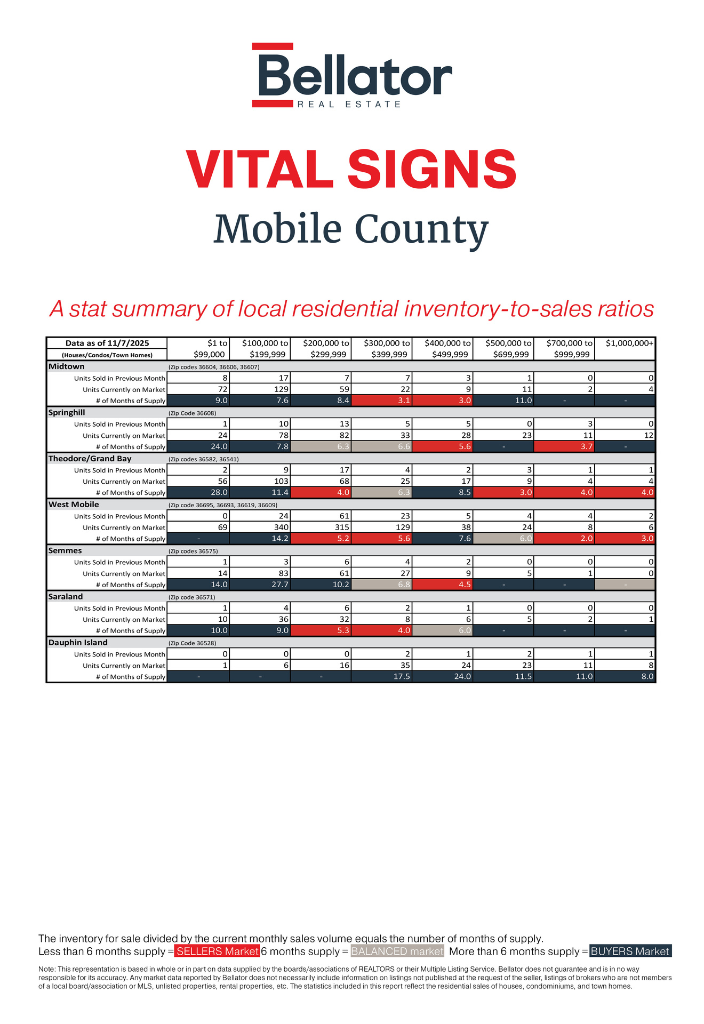

Mobile County Market Snapshot: September vs. October 2025

Housing activity in Mobile County showed subtle but notable shifts between September and October. Inventory levels remained stable across most submarkets, but sales trends reflected the typical seasonal slowdown, with the most balance appearing in mid-range price points. Entry-level and luxury segments, meanwhile, experienced more fluctuation as buyers and sellers adjusted to evolving demand patterns.

- Midtown

Midtown saw an uptick in sales activity in October, signaling renewed movement across a broad range of price points. The number of homes sold rose from 33 in September to 43, led by stronger performance under $200K. Months of supply declined in most categories—particularly between $100K–$300K, where supply eased from 9.9 and 4.9 months to 7.6 and 8.4 months, respectively. While inventory remains elevated overall, this improvement suggests a gradual rebalancing as buyers continue to pursue Midtown's affordable, centrally located options. - Spring Hill

Spring Hill maintained its steady pace through October, with total sales holding roughly consistent month over month. Supply in the $200K–$400K range shifted only slightly, staying between 6–7 months, while higher-end listings above $500K saw some volatility—the $700K–$999K segment improved to just 3.7 months of supply, reflecting stronger absorption of premium properties. This indicates continued buyer confidence in Spring Hill's established neighborhoods and desirable amenities. - Theodore & Grand Bay

In the southern corridor, Theodore and Grand Bay showed a mixed picture. While sales held firm in the $200K–$300K range, maintaining a balanced 4.0 months of supply, higher price points saw a rise in inventory. The $300K–$399K range climbed from 4.0 to 6.3 months of supply, suggesting slightly slower movement. Still, overall balance remains solid, particularly for homes priced under $400K, where demand continues to outpace available listings. - West Mobile

West Mobile remains one of the county's most active submarkets, driven by consistent buyer demand and a broad range of inventory. Homes in the $200K–$400K range remain highly competitive, with supply holding steady near 5–6 months, reflecting a balanced market. Interestingly, higher-end homes in the $500K - $699K range saw improved turnover, dropping from 29 months of supply in September to just 6 months in October, a strong indicator of selective but serious buyer activity in the upper tiers. - Semmes

Semmes experienced a modest cooling trend, especially in the $200K–$300K segment, where supply rose from 6.9 to 10.2 months, indicating slower absorption of listings. Despite this, lower price points continue to attract buyers seeking affordability in the western part of the county. Entry-level inventory remains limited, which could stabilize these numbers heading into winter. - Saraland

Saraland's market held steady into October, with little change in the $200K–$400K range—a consistent 4–5 months of supply signaling balance. Entry-level homes under $200K saw minor improvements as well, bringing supply closer to 9 months compared to September's 11 months. These trends suggest Saraland remains a resilient and stable submarket within North Mobile. - Dauphin Island

As expected, Dauphin Island reflected the seasonal slowdown typical for coastal markets entering fall. With fewer sales and steady listings, months of supply increased across several categories—particularly in the $400K–$500K range, where it rose from 10 to 24 months. However, island homes above $700K maintained relatively balanced absorption, holding between 8–11 months of supply. The slowdown aligns with off-season norms, with expectations for renewed activity in early spring.

Key Takeaways

- Mid-range homes ($200K–$400K) remain the most balanced segment countywide.

- Luxury listings above $700K saw selective strength in West Mobile and Spring Hill.

- Entry-level inventory remains tight in most areas, keeping first-time buyer demand steady.

- Seasonal cooling continues, especially in coastal and higher-end submarkets.

As Mobile County moves into the final stretch of 2025, the market shows signs of healthy normalization, maintaining activity across key price ranges while giving buyers more breathing room than in past years. With balanced conditions and steady absorption, both buyers and sellers can approach the winter market with confidence and strategy.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.

Privacy Policy / DMCA Notice / ADA Accessibility