Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

10

November 2025 Alabama Gulf Coast Real Estate Stats

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

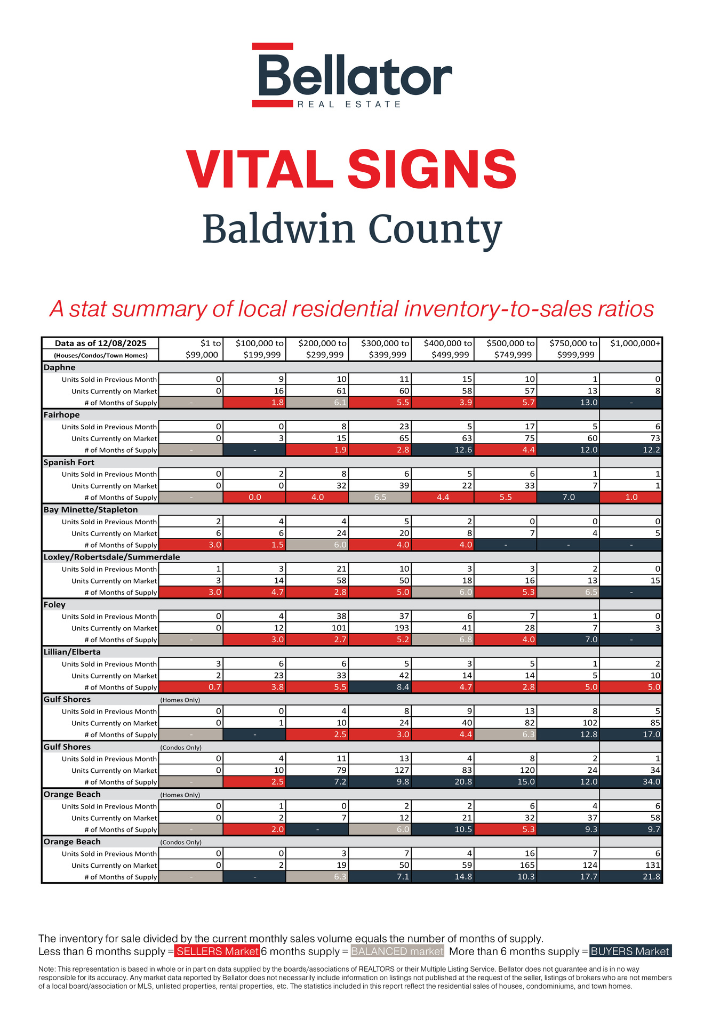

Baldwin County Market Comparison: October vs. November 2025

The Baldwin County real estate market continued its seasonal transition in November, with activity shifting from a brisk fall pace to a more balanced environment heading toward year-end. While some areas experienced fewer transactions, others saw notable increases in sales activity and lower months of supply—signaling strong demand. Across the board, the market remains healthy, particularly for well-priced properties between $200,000–$500,000.

Overall Market Themes

Sales Activity Held Steady, With Some Price Segments Improving

- Areas such as Daphne, Foley, and Loxley/Robertsdale/Summerdale saw higher or steady sales in November.

- Coastal markets—Gulf Shores and Orange Beach—saw mixed shifts, with single-family homes pacing more consistently than condominiums.

Inventory Remains Stable Across Most Cities

- Listings increased slightly in certain coastal areas, while suburban markets largely held steady.

- Months of supply improved in some segments, indicating good absorption of available inventory.

Balanced Market Conditions for Mid-Range Price Bands

- $200,000–$500,000 remains the most competitive price range in nearly every location.

- Luxury properties $750,000+ are seeing slower turnover, consistent with seasonal trends.

Highlights by Market Area

Daphne

- Sales shifted modestly by price point, but overall demand is holding steady.

- November supply levels remain healthy and balanced between 3–6 months.

What to know:

$399,000–$499,999 homes posted strong buyer demand, and the $750,000–$1M+ segment saw limited movement, typical for late fall.

Fairhope

- November saw slightly fewer total units sold, with notable adjustments in upper price brackets.

- Supply increased in the $400,000+ range, resulting in higher months of inventory.

Market takeaway:

Buyers have more choice than earlier in the fall, particularly from $400,000 and up.

Spanish Fort

- Sales softened in the $200,000–$400,000 price bands, while inventory stayed relatively steady.

- Months of supply increased, especially in the $300,000–$400,000 range.

Trend:

Spanish Fort is experiencing a seasonal shift to buyer balance, but opportunities remain strong for well-priced listings.

Foley

- One of the busiest markets in Baldwin County.

- Sales in November stayed strong, especially in the $200,000–$400,000 range.

- Months of supply are trending within balanced market levels.

Bottom line:

Foley continues to be a high-turnover, high-demand market.

Loxley / Robertsdale / Summerdale

- A stable and consistent market, with improved absorption from October to November.

- Months of supply dropped in certain price points, reflecting steady buyer interest.

Standout segment:

Homes in the $200,000–$300,000 bracket continue to sell efficiently.

Coastal Markets: Gulf Shores & Orange Beach

Gulf Shores

- Homes: Stable sales with manageable inventory; most price points remain between 2–6 months of supply.

- Condos: Higher months of supply, especially in the $400,000+, but activity remains present.

Key trend:

Single-family homes are pacing faster than condos as winter season approaches.

Orange Beach

- Homes: Slight cooling compared to October, especially under $300K, but activity continues in $500K–$750K and $1M+ at a slower pace.

- Condos: Inventory remains elevated, particularly in luxury segments.

Seasonal expectation:

Activity typically slows heading into December, with stronger momentum returning in Q1.

Price Band Observations

- $200,000–$400,000 remains the most active range, countywide.

- Luxury listings ($750,000+) show longer days on market heading into winter, consistent with historical patterns.

- Affordable inventory below $200,000 is scarce in most communities.

Key Takeaways for Buyers & Sellers

For Buyers

- Good opportunities exist in Fairhope, Spanish Fort, and coastal condos, thanks to slightly higher inventory.

- Rates and pricing are steady — the window for winter bargains is opening.

For Sellers

- Listings priced between $250,000–$500,000 continue to move efficiently.

- Presentation and pricing remain critical in upper price points.

Closing Outlook

As Baldwin County heads into winter, the market is displaying healthy moderation and seasonal balance. Core residential neighborhoods continue to perform well, while luxury and coastal sectors experience typical softening. With stable inventory levels and steady demand in the mid-range price points, Baldwin County remains an attractive market moving into 2026.

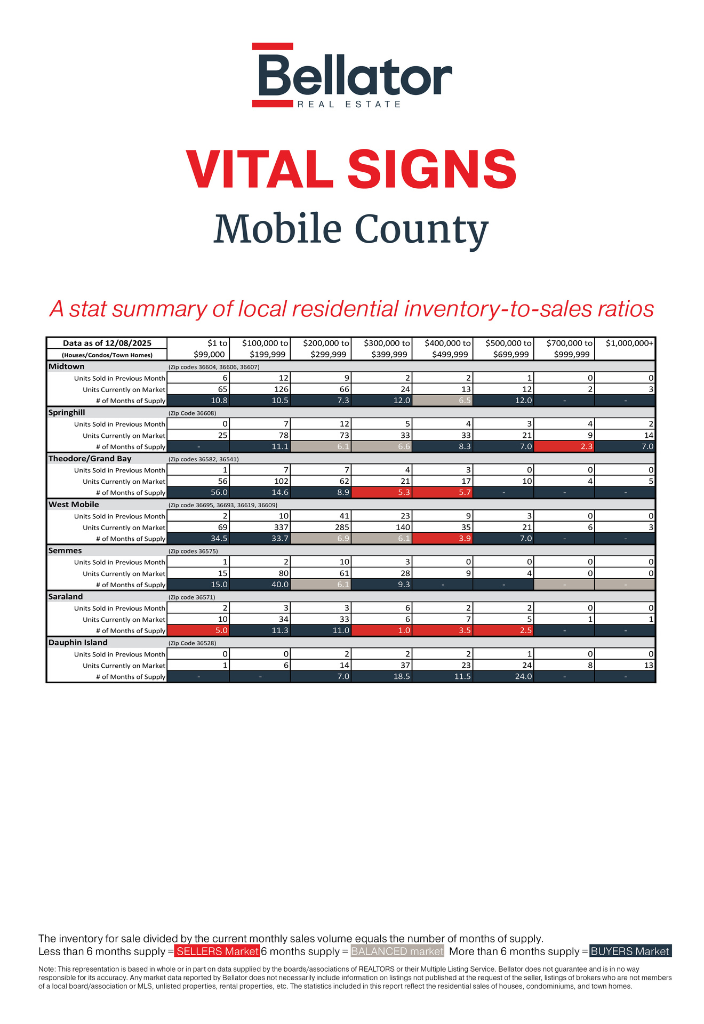

Mobile County Market Comparison: October vs. November 2025

Mobile County experienced a noticeable seasonal slowdown in November, with sales activity easing across most areas and price points. Inventory levels held fairly steady, but months of supply increased in several neighborhoods, especially where fewer properties sold. Despite softer demand, the market remains active in affordable and mid-range price brackets—particularly between $200,000–$400,000.

Overall Themes

Sales Activity Slowed in Most Neighborhoods

- Midtown, Theodore/Grand Bay, and West Mobile all posted fewer units sold in November.

- Dauphin Island, Saraland, Semmes, and Springhill saw equal or improved activity in select price segments.

Months of Supply Rose in Key Areas

- Areas with fewer November sales saw significant jumps in months of inventory.

- This points to a more pronounced seasonal transition as buyers paused heading into the holidays.

$200,000–$400,000 Remains the Most Active Price Range

- Despite slowing, these price bands continue to see the most movement countywide.

- Properties priced under $200,000 and over $700,000 remain slower to turn.

Highlights by Market Area

Midtown (36604, 36606, 36607)

What changed:

- Sales decreased in nearly every price band.

- Months of supply increased notably in the $100K–$200K and $300K–$400K ranges.

- Supply rose from 8–9 months to 10–12 months, indicating slower absorption.

Market implications:

Midtown is seeing a seasonal pause, but inventory remains manageable for buyers seeking older homes and character properties.

Springhill (36608)

Sales softened at the lower price points, while luxury activity increased slightly.

- Upper-price segments ($700K–$1M+) saw more sales than in October.

- Months of supply improved for some ranges but rose in others due to changes in active inventory.

Springhill remains healthy, but more balanced — particularly in $300K–$500K.

Theodore / Grand Bay (36582, 36541)

This area saw the largest slowdown in November.

- Sales dropped sharply in multiple price bands.

- Months of supply spiked, with certain ranges reaching 14–56 months of supply due to very low turnover.

This is a seasonal stall, and activity should pick back up in spring.

West Mobile (36695, 36693, 36619, 36609)

West Mobile typically leads the county in volume—and November showed:

- Sales down in most ranges, especially $200–$300K.

- Months of supply rose in several price bands, now trending around 6–7 months in key ranges.

The area remains balanced, but autumn momentum has eased.

Semmes (36575)

Semmes saw a mixed month:

- Sales improved in the $200K–$300K range.

- Activity dropped in the entry-level and upper-mid ranges.

Months of supply continued into double digits in some segments.

Saraland (36571)

Saraland was a standout performer.

- Sales increased in the $300K–$400K range.

- Months of supply fell sharply in multiple price bands, with 1–5 months in key segments.

This is one of the strongest markets in November — efficient turnover, steady demand.

Dauphin Island (36528)

- Seasonal second-home and condo trends are clearly visible.

- Months of supply remains very high, especially $400,000+.

Activity is typical for late fall:

Luxury and coastal inventory is sitting longer, which aligns with seasonal patterns.

Price Band Observations Across Mobile County

- $200,000–$400,000 continues to be the backbone of the market.

- Inventory is building in entry-level and luxury segments, where buyers tend to slow during holidays.

- Balanced markets persist, especially in Saraland and West Mobile, where sales keep absorption strong.

Key Takeaways

For Buyers

- More options are available—especially in Midtown and Springhill.

- Winter could offer negotiation opportunities, particularly in higher price bands.

For Sellers

- Homes priced from $200,000–$400,000 are still moving efficiently.

- Correct pricing and good presentation are essential in luxury and coastal segments.

Closing Outlook

Mobile County is transitioning into its winter mode, with reduced activity after a strong fall. Inventory levels remain stable, and the market is still performing well in mid-range price points. As we move into early 2026, expect activity to pick back up—especially in Saraland, West Mobile, and affordable ranges.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.

Privacy Policy / DMCA Notice / ADA Accessibility